24 / 110

24 / 110

24 // iberian.propery / 2017

dossier// ISSUE: TOP IBERIAN Investors

For the first half of 2017 propertymarkets in Iberia

have continued to perform strongly, supported

by an economic recovery that is driving increases

in occupancy rates and rental levels. GDPgrowth

forecasts remain positive: 2.0% for Spain, 1.2% for

Portugal for the period 2017-21, remarking the

different paces of both countries but with com-

mon features such as improvements in internal

demand and falling unemployment.

In this context, international capital continues to

flow into Iberia. Investors remain attracted to Span-

ish and Portuguese real estate, as both countries

still offer rental growth prospects and an attractive

yield premium over other markets in Europe.

There are, however, some challenges that in-

vestors are facingwhen building up their Iberian

portfolios. Perhaps the most relevant has to

do with the access to quality product, which

is becoming difficult and competitive as the

existing available stock is not enough to satisfy

an increasing demand. In order to overcome

this, investors need the support of strong local

teams and partners who are able to identify the

right product/opportunities that will help them

to execute their investment strategies.

Another consideration is that as yield com-

pression has already taken place and rental

growth is priced into property values, the skills

and ability of the Asset Management teams to

execute business plans in accordance to under-

writing assumptions and identifying new levers

for growthwill become key to extract value from

the portfolios and deliver performance.

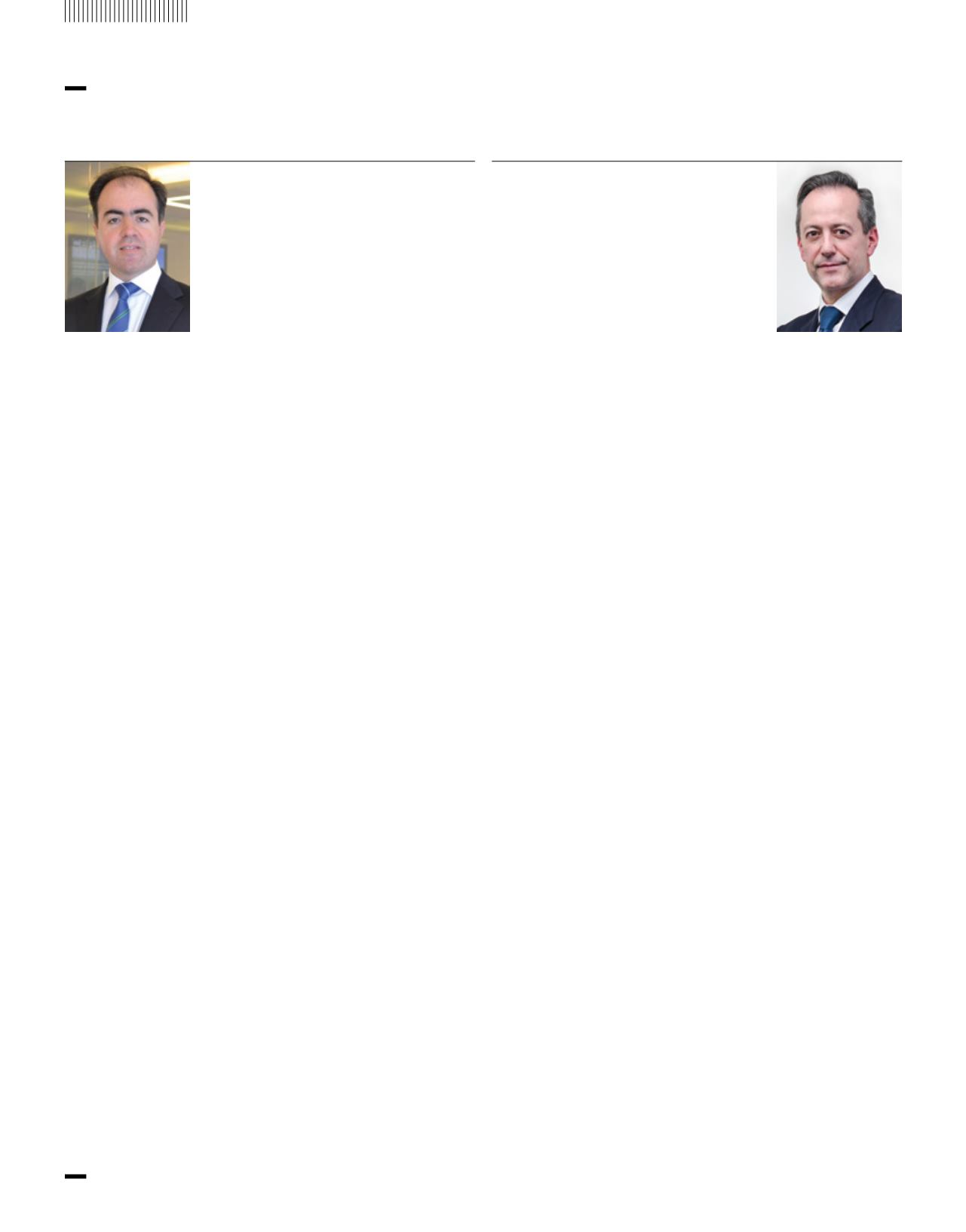

Antonio

Simontalero

CBRE Global

Investors

Head of Investment

Operations Iberia

During the first years following the crisis, many

opportunistic deals were made in the Iberian

market, but the establishment of Socimis gave

way to more value-added and core plus deals,

due to the their different returns requirement

and the great number of deals closed.

Today, the challenges will depend on the type

of return required. Opportunistic has become

more difficult, unless new projects are devel-

oped, namely residential projects where some

of the key players have already been accu-

mulating land at good prices. Sareb in Spain

and banks in general continue to have a heavy

balance sheet that will lead to opportunistic

sales, but the challenge is to obtain defined

portfolios from them.

Tourism in the Iberian Peninsula has risen

considerably in the past years. There is still

a great number of hotels or hotel portfolios

that belong to individuals who do not plan to

continue the business, and the longstanding

lack of investment in these assets makes them

suitable for rebranding and refurbishing with

international operators. The challenge will be to

identify this type of opportunity and convince

the seller of this strategy.

It is still difficult for the core pockets, but it will

come in the short time.

Developing a pan-Iberian strategy has been

easier for the Socimis and similar structures

due to their required returns and type of invest-

ment. To develop a truly pan-Iberian strategy it

is helpful to be represented in both countries,

either by affiliates or operating partners with a

good local presence and knowledge.

Pedro Abella

Langa

H.I.G. European

Capital Partners

Principal