Investors attending the "Why Iberia?" raise their hand: it's time to buy!

Iberian Property and Real Asset Media gathered once more the investment community in London. The “Why Iberia?” conference returned to the Nuveen headquarters in London, this Wednesday (28th of June) in a half-day format event, where the discussion focused on the latest research, strategies, and local market insights for Spain and Portugal.

During the opening remarks Richard Betts, Group Publisher at Real Asset Media, shared how after the 2008 financial crisis people though Iberia would not be on investors radar, which now proves to be far away from reality…people do want to invest in Spain & Portugal!

For its part, António Gil Machado, Director at Iberian Property, introduced some of the main key figures for the Spanish and Portuguese economies. The GDP growth stands out in both countries (Spain registering a 2% yearly growth, and Portugal 2,5%), mainly driven by exports; the government balance is still beyond desired, but debt is expected to be reduced; and so far 2023 is beating 2019 tourism levels, which is also being one of the growth motors for both economies.

Valdecarros Madrid – one of the largest urban development projects in Spain

Luis Roca de Togores, President of the Valdecarros Community Council, explained the audience how Valdecarros has accelerated in a particularly turbulent economic and political context, both internationally and domestically. Nonetheless, the Spanish economy grew by 0.5% in the first quarter of the year, compared with the 0.1% of the Eurozone. Spain has become well placed to lead economic growth over the next two years among the large-developed countries. The latest forecasts published by the European Commission and the IMF already placed the Spanish economy in the lead, as also confirmed by the OECD, raising the growth forecast to 2.1% in 2023 and 1.9% in 2024.

Spain has also ranked fourth among the most attractive European destinations for property investment, climbing three places from last year and only lagging behind the UK, Germany and France. Due to its legal security and tax advantages, Madrid in particular is one of the most sought-after cities in Europe for investing.

Three months ago, Madrid City Council approved the adaptation of the Valdecarros enabling works project to its execution, with a total budget of 1.8 billion euros, in eight stages. If we add the construction investments, this new Madrid neighbourhood will contribute more than 7.5 billion euros to Madrid and will create some 450,000 jobs.

Of these eight urban development phases, the first one is already underway since 2021 and the works for the second and third ones will begin shortly.

In the 16 years planned for the full development of the eight phases, a total of 51,000 new homes will be built, a third of the 150,000 planned for the entire capital over the same period. Of those 51,000, at least 55% will be under some form of price protection, so this new neighbourhood will henceforth be the epicentre of affordable housing in the city. In this regard, Valdecarros will provide the largest new housing stock in Madrid for the next two decades. It will be Madrid’s most inhabited and with the highest density of services and green areas neighbourhood.

“Public-private collaboration, proper urban planning and a comprehensive, stage-by-stage development such as ours make the best contribution to improving accessibility to housing, which is so badly needed by everyone and especially by young people”, stated Luis Roca de Togores.

Valdecarros' strong investment appeal and four recent awards led to a successful first round of residential plots auctions, where major developers bid remotely for three plots, with prices reaching up to €1,100/sqm for free-price housing.

The developers Habitat and Aedas were awarded the aforementioned plots, an addition to those that had previously joined the project (Azora, Ebrosa, Pryconsa, Zapata, Hermanos Santos and Oncisa) and the financial institutions that also own land, such as Banco Santander or Sareb. These owners are also joined by local and regional authorities, which altogether will build 36% of the homes.

As the epicentre of developments in the south-east, Valdecarros will also be instrumental in defining a new intra-urban mobility and a structure of premium-quality amenities.

The effort of Valdecarros in sustainable mobility is truly one of the differentiating elements in the sector. 70% of streets have a slope of less than 2%, a percentage that rises to 86% if we consider slopes of less than 3%. Adapting the roadways and plots to these slopes, represented an additional cost of approximately 249 million euros. In all likelihood, this is the flattest area of the entire capital, an invitation to move around on foot. This will make a very significant contribution to a district that is not just more sustainable but also much healthier.

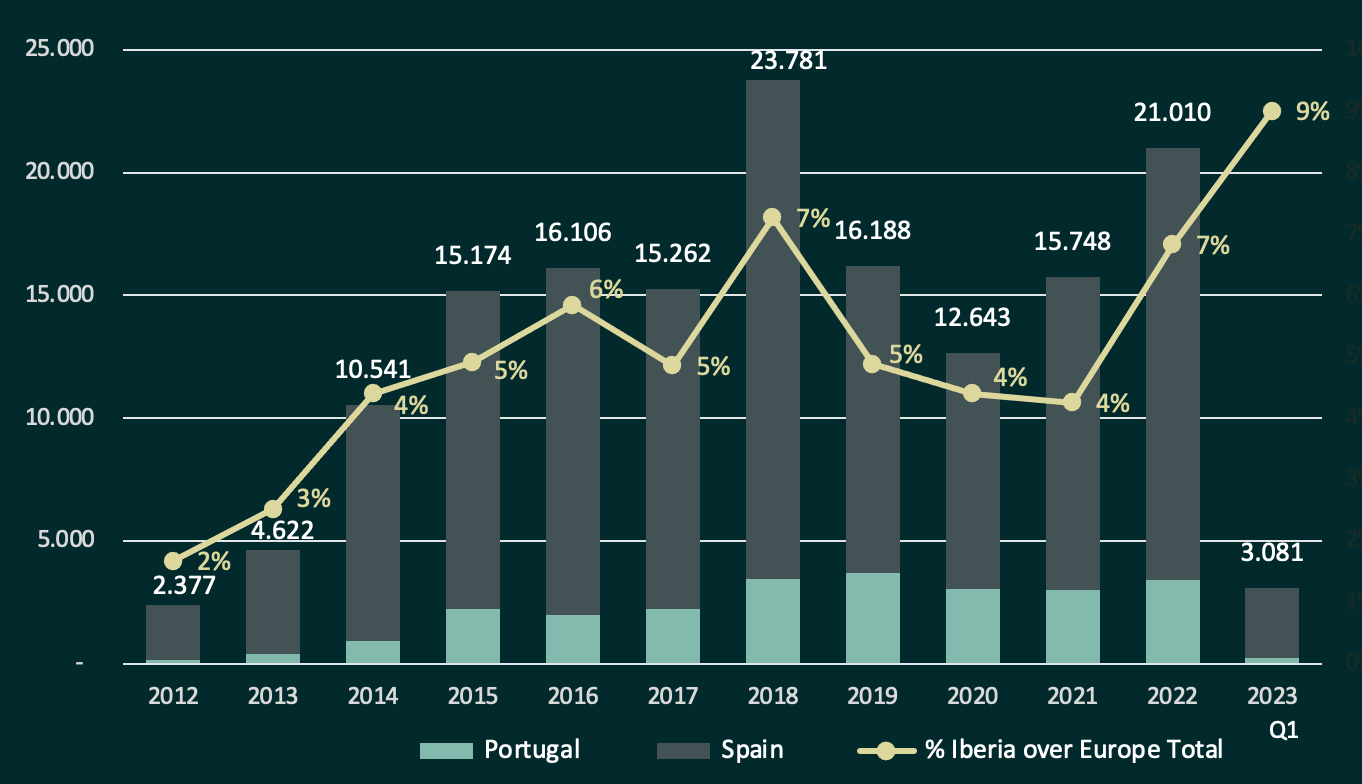

Record of Iberian investment contribution to Europe

Following the macro & real estate economic outlook, Carlos García Redondo, Senior Director Investment Properties I&L at CBRE Spain, and Nuno Nunes, Head of Capital Markets at CBRE Portugal, have jointly presented the latest research insights for Iberia.

Portugal and Spain are growing more than most European countries. Although tourism keeps being a positive boost, there has been a very positive development in other sectors such as manufacturing and other industrial activities. On the other hand, public investment has also increase positively, which is something that hopefully will remain being fed into the economy in the next few years.

Regarding the general sentiment of the sector, the fast interest rate hike is a known issue, and it explains a big part of why the market is so still, or why the investment volumes can decrease significantly this year. On Nuno Nunes words “a significant portion of the market is still trying to understand how to accommodate this shift into their current valuations, into their new investment programme”.

Carlos García Redondo agreed on the subject and reinforced that “almost 100% of Institutional investors need financing and this factor is critical for them, these forces of hike of the last 300 days it's taking time to time to adapt… and even for the for investors who don't take financing, they are still trying to understand what the correct pricing is, and no one wants to be catch falling”.

With one semester to go, it's more or less clear that we won't see the same investment volumes as we had last year or many years before that, and in fact for the European market as a whole the general sentiment is that we can be back to the levels of 2012/2013. However, Nuno Nunes points out the silver lining – Iberia investment volumes and the interest it has collected from international investors has increased significantly, and for the first time over the last 10 years Iberian investment is almost 10% of the total European volume, being the majority done by Spain.

In the first quarter of 2023 Iberian investment volume has been reduced by roughly 30%. In Spain we saw a 3 billion volume led by the living sector and offices, which has been unusually driven by a single portfolio deal of 3 buildings worth 300 million, bought by a domestic investor. For Carlos García Redondo, the surprise lies within the third position being occupied by retail, even from a European investment volumes perspective.

In this sense, Nuno Nunes commented “retail starts to be one of the hidden gems, here for the long time, and now in relative terms offering very interesting risk adjusted returns”.

Investors move to a more tactical approach

In Spain, institutional investors are changing to a tactical approach being more open to do smaller operations. With regards to the investor origin in the first quarter 2023 the most active were domestic investors, followed by the Americans and French.

In Portugal, local players are a lot more active, but they are doing smaller deals. On the other hand, international investors are doing only a handful number of operations but with higher tickets.

Nuno Nunes shared that there is an important number of new investors looking into the market and “we will probably see a few number of operations from them in the remainder of the year. At the moment, it is kind of difficult to do deals above 50 million, and up north the 100 million it’s a very tight space but dropping to the range between the €20 and €50 million the market keeps being very dynamic”.

Where are the returns? Segments analysis

António Gil Machado kicked-off the roundtable discussion that followed with a simple question: by a show of hands, the majority of the audience present in the room defended that it is time to keep buying real estate assets, and only a few believed it was time to retain their investments, a similar feeling to the one registered in the 2022 conference.

Siena Golan, Real Estate Research Analyst at DWS, started by differentiating the performance of the occupational and investment markets.

Regarding the first one, offices were highlighted as the uncertain segment where employment growth is being translated into a strong take-up, with Iberia having a higher physical occupancy than rest of Europe – Madrid is around 65%, which compares to below 50% physical occupancy in CEE. Still, Siena Golan believes that “the most compelling story lies on the living segment, where a huge demand confronts many years of inadequate supply”. The household composition in Madrid is above the eurozone average (3 vs 2.5 persons per house), and in the next 10 years this figure is expected to converge, which would translate in another source of demand growth.

On the investment side, ECB maintaining its policy of raising rates means we are going to see falling capital values. DWS portfolio biggest holding is in retail, however over the last three years the Deutsch Bank real estate investment branch (DWS) has placed its focus on residential, building a portfolio of over 3,000 beds. For Siena Golan, “affordable housing is the most interesting opportunity, it seems like there is a real political will to increase the supply, and the model for public-private partnership in the sector is quite interesting in Spain”.

Where are the returns? Cities analysis

Spain is a big country, with many big cities. Madrid has benefitted in the recent years from a very pro-business government (both in community and city), Barcelona went through a more struggling environment, and secondary cities like Valencia, Malaga, and Bilbao seem to be rising… so where do investors feel more confident to invest in?

On Carlos García Redondo view, when investors come to Iberia they take into account the macroeconomic figures, “and when they land in Iberia, they almost pretend to buy first in the main cities like Madrid and Barcelona, but they are really focusing more on concrete cities with strong fundamentals and available opportunities, instead of looking to the country scale”.

In the case of Portugal there still appears to be only one city comparing to the Spanish ones – Lisbon. Porto, the second biggest city of the country, is performing quite well on the occupational side, and it's clearly in the radar of international occupiers, especially for offices, although Nuno Nunes shared that there is also movement from logistics and hotels operators. Nonetheless, “for international investors Porto still doesn't rank at the same level as Lisbon, which is understandable due to their different sizes, and visibility”.

“Madrid has a very different dimension and capacity to attract not only investors as also tenants, but in the last few years Lisbon has surpassed Barcelona as an investment destination”, concluded Nuno Nunes.

“Barcelona political will to regulate rents in the residential sector has resulted in an office oversupply”

Siena Golan closed the roundtable discussion with a ‘weather forecast’, identifying clouds over Barcelona, where the political situation is not very helpful for investment.

Consequence of the regional government being very keen to regulate rents in the residential sector, in recent years new supply was pretty much choked off, with a reduced ability for investors to realise good returns.

“Whilst you have this political will to control rents in the sector, the market became less active and as a result some developers have been moving away from the residential road towards offices resulting in an oversupply of office space, particularly in the new business areas”, stated the Research Analyst from DWS.

Legal & Tax update for Spain

To provide insights on the Spanish regulation, Carlos Portocarrero, Partner at Clifford Chance and Fernando Escribano, Counsel (Tax) at Clifford Chance, prepared a joint presentation, whose highlights we share below.

Things to be considered when you invest in Spain from a legal standpoint:

- Legal system – since we were invaded by the Romans 25 centuries ago the legal system has basically remained the same, being very solid and stable.

- Spain, part of the European Union –there's a limit to what the government can do or can’t, and there's a common regulation across Europe that applies to Spain, like data protection, anti-money laundering, etc., presenting similar features to other jurisdictions inside the EU.

- Foreign investment requires approval – assets which are considered sensitive, or even concessions require a special proceeding to apply for authorisation.

- Consumers are heavily regulated in Spain – when buying retail, offices and logistics there are no issues, but when investing for example in BTR consumers regulation must be taken into account (same applies for BTS).

- New housing law – “being the flavour of the month, we don't know if it's going to change, considering we have general elections in July…however, even if the conservative party comes to power, I doubt that they will just abolish the law”.

Regarding the last topic, Carlos Portocarrero commented that we have seen all across Europe rent controls caps, and that to some extent for the ones who are invested already it could be good news. He explains “some of the housing will be out of the leasing market due to this measure, so the reduced supply will put more pressure on prices, which is good for the ones who already own the houses”.

Development may be affected a little bit, but it’s a matter of putting a number to what the cost of those rental caps is (if they finally come into force), particularly in Barcelona, as Madrid is inclined to not applying that law.

For its part, Fernando Escribano shared some views on the type of vehicles to be chosen based on acquisition model (asset vs. shares), holding period, and income tax.

When private investors want to acquire real estate in Spain the HoldCo-PropCo brackets are the ones usually to be assessed as “they are the quicker swan, but they have some cons like rental income being taxed at ordinary rate, which is currently 25% corporate income tax rate. As for the pros dividends capital gains are only taxed at effective 1.25%”.

On the other hand, for investors who are not focused on commercial real estate and want instead to invest in housing an EDAV (entities devoted to the lease of dwellings) may be a good option. The main advantage is their reduced VAT rate: 4% against the 10% which would apply to any ordinary investor. Should be noted that this vehicle does not protect the capital gain, so investors really need to balance where the yield is for them.

“If the investors are here for the long run, and they want to the devote the assets to be leased the vehicle is clearly the Spanish REIT”, revealed Fernando Escribano. Socimi is the vehicle which allows the investor to have a 0% corporate income tax rate on rental income, subject to a minimum 10% taxation requirement at the shareholder level. As for the cons, the assets have to be ‘qualifying assets’, meaning that they must be urban assets to be leased for at least three years. An additional con, which nowadays is less a problem, is the listing requirement of the vehicle. Until a couple of months ago there was a free flow requirement, which for the private investors was not so pleasant since they don't want to share their yield with ordinary external people, but recently a new market was approved in Spain and free flow is not required.

Legal & Tax update for Portugal

Following the same model, João Torroaes Valente, Partner at Morais Leitão and Paulo Núncio, Partner at Morais Leitão, shared some insights on the latest Portuguese regulation updates.

The last major legislative measures taken in Portugal target the residential sector. The government has taken measures following the assumption that Portugal has scarce housing offer, and a problem related to increasing rents in the city centres due to the tourism and local lodging industry. Like so, since February of this year, a legislative reform was outlined (currently in the parliament) to stimulate investment in the residential sector, stimulating residential leasing and affordable housing.

João Torroaes Valente underlined the jewel of this reform as being the ‘simplex’ - the simplification in terms of licencing. The first goal is to increase the number of exemptions into the licencing, meaning the majority ofurban planning operations will become either exempt or only based on the liability of the project, instead of having control mechanisms by the municipality. “As a result, there will cease the obligation to have titles for the permits, the need to obtain construction permit and use permit for the buildings will be substituted by the project liability, and the payment of the necessary charges due to the municipalities…which we believe will pose as a revolution in terms of licencing speed”. A simplification in terms of documentation is also expected – there will be an electronic platform for the whole country whereby you can access the exact situation of each project, in each municipality (expected to be completed by 2024).

Additionaly, the government proposal also intends to limit the local lodging registration or permits for five years, with new registration being suspended. Both the Lisbon and Oporto municipalities have already announced that they will not apply this measure, and therefore they will introduce regulations that are foreseen also in this bill of law.

Finally, the large buzz that resulted from the law is the compulsory leasing that the government has introduced in cases where property owners have vacant properties for more than x years. Morais Leitão believes this measure is doomed to be non-compliant with the constitution due to the violation of some constitutional principles like the property ownership, and thus that the measure should not be approved.

Paulo Núncio, in charge of clarifying the tax impact of this law, began to recall that one of the most important parts of this new bill refers to the short-term rentals. In this matter, the government goal is to force the owners of residential properties, currently allocated to short-term rentals, to rent them under long-term rental markets. And to that end, the bill provides an extraordinary tax contribution applicable both to individuals and corporations, that list those properties in AirBnb and similar platforms (this extraordinary tax contribution will be applicable on top of personal income tax or corporate income tax).

Additionally, in order to promote and encourage the relocation of residential properties, the government is going to implement an exemption from income tax until 2029 on rents collected under long-term rental agreements on the residential properties that were previously used for short term rentals. Also worth mentioning is the new income tax exemption on gains that provide from the sale of residential properties to the state.

Finally, this law also foresees an exemption from property tax on land for construction of residential buildings, and on residential buildings whose licence procedure is pending approval.

Build to Rent, the new formula for residential investment!

After a coffee-break where participants had the opportunity to network, Javier Martin, Senior Portfolio Manager at Nuveen Iberia, kicked-off the second half of the conference pitching for a specific opportunity to invest: the Build-to-Rent (BTR) segment.

Nuveen has been investing in the BTR model through a joint venture with Kronos, which gave origin to the STAY brand. Madrid, Barcelona, Valencia, Cordoba, and Tarragona are some of the locations where the vehicle identified strong fundamentals, and thus invested already.

Javier Martin started by exposing the occupier market problems, being the imbalance between demand and supply the main one. The shortage of supply results in a pressure over rents, conditioning the access to affordable housing in the big cities. To this, should be also summed the scarcity of land to develop and the increased construction costs.

As for the current supply on the rental market, two factors stand out: 95% of the households are owned by individuals, and only 5% owned by institutional investors, translating into a segment with lack of professionalization; the stock providing from individuals is usually outdated, lacking amenities, with no ESG concerns, and with managing inefficiencies…but still at very similar prices to the new quality stock.

Following this data, Javier Martin defended that “institutional investors have a wide range of margin and possibilities to invest in Build to Rent, during Q1 2023 the segment captured around 805 million euros investment, and last year we saw already a record investment”. Besides, he also commented that the correction on yields has been well less noticed when compared to other segments.

Political activity remains an area of concern, as many of the measures seem to be displaced with the sector reality, thus not really offering solutions. This is the case of the 90,000 affordable housing units promised to enter the market: 50,000 from Sareb, and 40,000 houses to be financed by European funds for construction. Javier Martin called out that “the 50,000 units from Sareb are located in what we call ghost locations, in areas with no demand for renting, and almost half of them are occupied illegally”.

On the positive side, the increasing effort rate to buy a house, together with cultural changes, keeps pushing demand for the renting market. And there are opportunities not only in Madrid and Barcelona, but also in regions like Valencia and Malaga. Like so, from Nuveen they explain that Tarragona is one their success cases in demand identification: petrochemical companies represented a very significant niche market for renting houses, which led to a 100% pre-let promotion developed there, under the STAY brand.

Over the next two years Nuveen expects to reach a total investment of 1 billion euros in the Build to Rent segment, being currently at 700 million euros.

Where is “Alpha” for a diversified portfolio in Spain & Portugal?

Fernando Ferreira, Chief Investment Officer at Square Asset Management, oversaw providing insights on where is the “Alpha” for a diversified portfolio in Iberia.

In an entertaining approach, Fernando Ferreira challenged ChatGPT to help him answer the question, and the result was very interesting. “Besides all the themes mentioned already during the conference, for me the thing that caught more my attention is the mentioning of retail, which can only mean the algorithm has found a large source of information that retail is is back!”.

Square Asset Management also asked the main agents in the market to share their wisdom on where the market is heading this year.

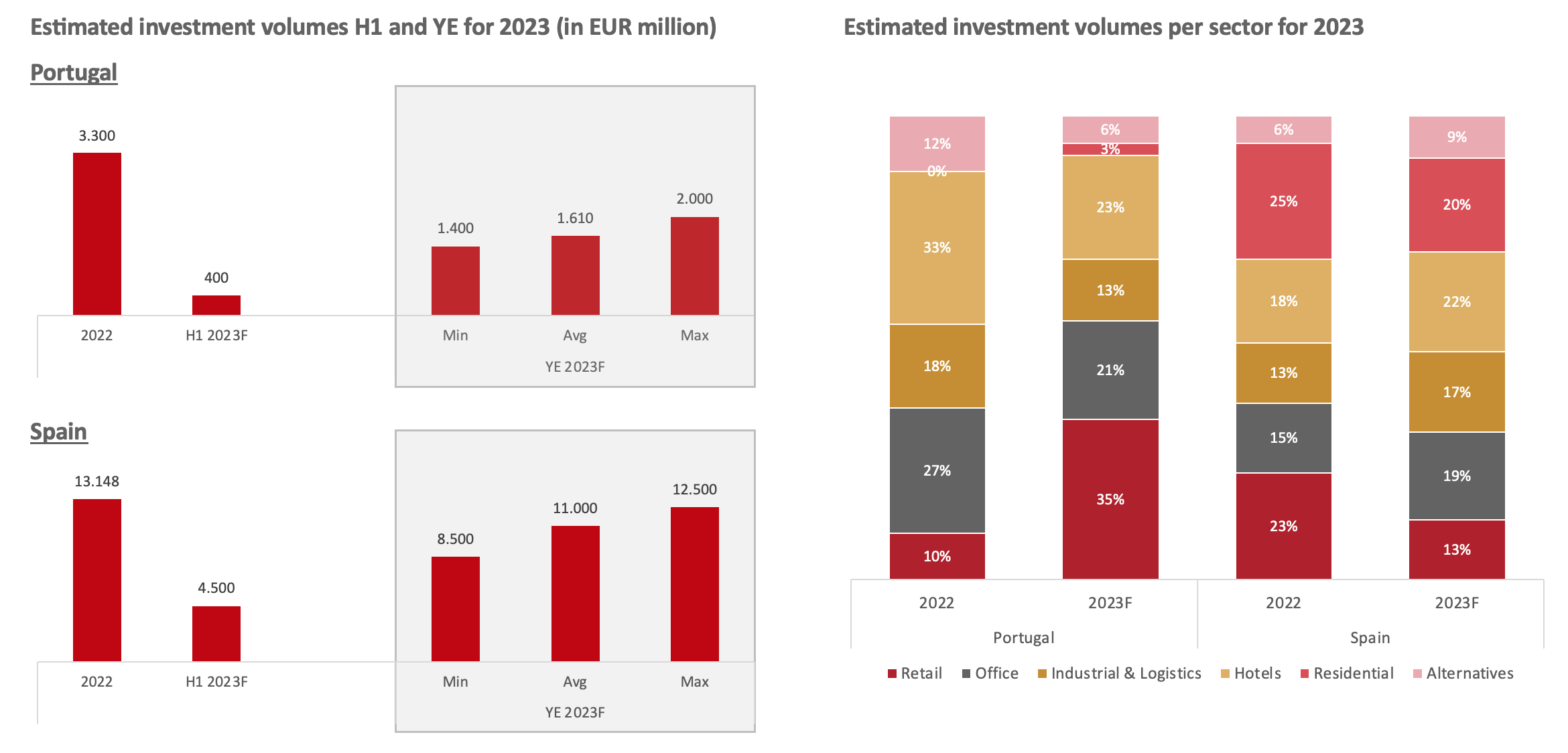

For Portugal, the conservative estimates place the investment volume at 1.4 billion, while the most optimistic at 2 billion (with the average at 1.6 billion). This means that the market will need to perform in the second half of the year 2/3 times more than what it has performed so far.

Equally to Portugal, even the optimistic estimates for Spain represent an y-o-y decrease of the investment volume, as can see in the image below.

Moving on to the rent adjustments, all sectors across Portugal and Spain seem to go an upward movement, especially on the residential segment. There is still an incognita to where offices might end up, “but in the case of Lisbon for example, there is still poor stock linked to the many years of financial prices constraining development activity – thus, for the new stock there's a premium that tenants are willing to pay”.

Fernando Ferreira also shared Square Asset Management strategy. With around 1.7 billion euros of assets across Spain and Portugal, the private owned investment manager is quite diversified, investing in several asset classes. The Spanish proportion is still quite small, because of the 18 years the fund celebrates this month, only the last two marked the exposure to the Spanish market.

In terms of the sector dispersion, NOI (Net Operating Income) marks the path. “We are not the investors that will be buying the best office building in Madrid at 4,5% or 5% yield… we are focused on getting returns to our unitholders, which means that our entry point needs to be somewhere north of 6,5% to 7% for the best assets”. This, Fernando Ferreira explains, is one of the reasons why Square AM has been investing in secondary locations – “if there's a building in a certain location that makes sense for a operator, willing to enter with a long-term lease, then we will go for it no matter how shiny that building is”.

A warm thank-you

There was still time for a last roundtable discussion, moderated by Richard Betts, that counted with the participation of Javier Martin, Fernando Ferreira, Siena Golan, Carlos García Redondo, and Nuno Nunes.

At the conference closing remarks, António Gil Machado and Richard Betts took the opportunity to thank Nuveen for hosting once again in their London headquarters this half-day conference focused on Iberia. Thanks to the support of Nuveen Real Estate, Square Asset Management, Valdecarros Madrid, CBRE, Clifford Chance, and Morais Leitão, the real estate investment community was gathered in London, enjoying high-level content on the 28th of June.

ACCESS HERE ALL PRESENTATIONS:

- Spain & Portugal – the macro & real estate economic outlook, by CBRE

- Legal & Tax update for Spain. What should you know?, by Clifford Chance

- Legal & Tax update for Portugal. What should you know?, by Morais Leitão

- Build to Rent, the new formula for residential investment!, by Nuveen Real Estate

- Where is “Alpha” for a diversified portfolio in Spain & Portugal?, by Square Asset Management