74 / 110

74 / 110

74 // iberian.propery / 2017

dossier// ISSUE: TOP IBERIAN Investors

The main challenges that face investors in the

Iberian market involve above all: the need to as-

sess investment intentions within a competitive

context, where the time needed to evaluate an

investment opportunity correctly may conflict

with the availability to carry out the investment

intentions; predicting the reversal of the market

trend; and the fact that the available indica-

tors (namely rental values applied in the office

markets) do not reflect the market reality. I will

explain this last point using the practical exam-

ple of the office market in Lisbon: the market

indicators for prime rents do not reflect the ac-

tual prime rents practised because the buildings

where these are being applied display physical

characteristics that raise doubt regarding their

classification as “

prime

” due to their age and con-

dition. This situation is a consequence of a lack

of investment in the office market, aggravated

by the fact that, from the pipeline for the next

two years (approximately 58.000 m2), only 25%

(11.000 m2) of the areas are currently available.

It would be much easier to define a pan-Iberian

strategic plan if there was more awareness re-

garding the specificities of each market, and in

this sense I amnot distinguishing countries, Spain

or Portugal, but cities (Madrid, Barcelona and

Lisbon). The strategy should also include cities

where investment is not as obvious due to a lack

of indicators – such as the city of Porto – but that

are experiencing great momentum and growth.

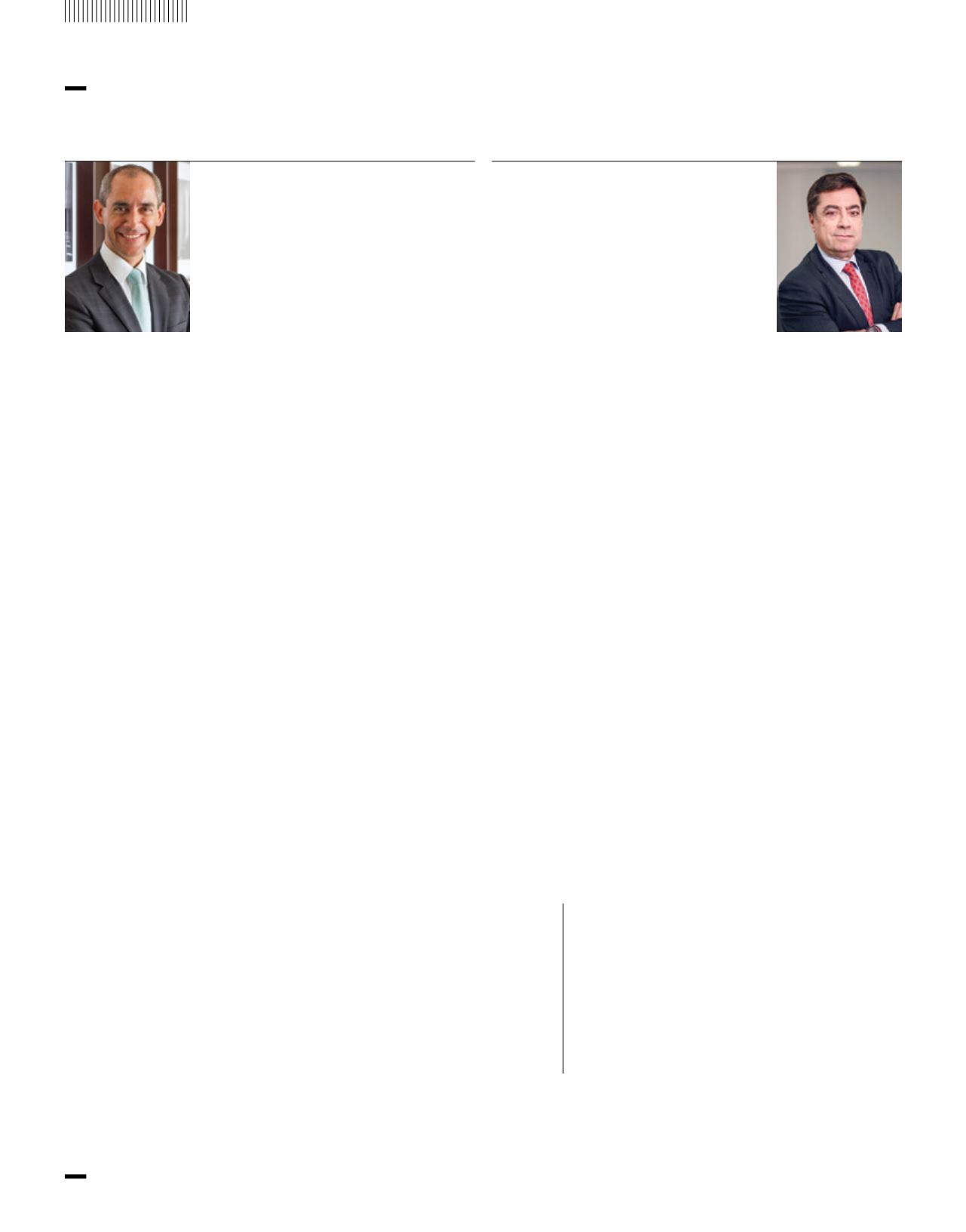

Paulo Silva

Aguirre

Newman

Managing Director

Spain is undoubtedly an appealing country for

international and national investors in the real

estate industry. Only in 1Q 2017, around €3.8

billion have been invested in our country, a figure

in line with those achieved in 2016 and 2015.

But where, how and why is it being invested?

In addition to the more “

traditional

” assets such

as retail, office, logistics or residential assets,

other types of properties -so-called alternative

assets- are emerging. These include hospitals,

student residences or elderly homes, especially

the latter type. The returns on these businesses

are not as high as on other real estate assets,

although they are sustainable and -due to de-

mographic reasons- their demandwill not stop

growing in the coming years.

In Spain, these centres have traditionally been

managed by families or religious institutions,

and little by little, both national and interna-

tional investors specializing in the manage-

ment of these assets have started to acquire

and build them not only in a region or specific

area but all over the country, in search of a

considerable volume making efficiency pos-

sible in terms of staff management, resources

and beds. These funds, whether pension or

mutual funds, provide capital and manage-

ment and search for these assets capable of

providing a 4.5-6.0% return rate. In fact, only in

2017 the total amount invested on these assets

is expected to reach €750 million.

Luis Martín Guirado

Gesvalt

Corporate Director

of Business

Development

Alternative

Assets, the new

focus of real

estate investment