SPAIN GAINS INFLUENCE IN THE NEW INTERNATIONAL REAL ESTATE LANDSCAPE

Spain Real Estate Summit - 2026

On the 5th and 6th of May, Iberian Property brought back to Madrid the key event for all who are already investing or contemplating to do so in the Spanish real estate sector. In the 2026 edition of the Spain Real Estate Summit, the global property sector was well represented by over 300 industry leaders from a wide range of countries, such as Spain, Portugal, France, Germany, Italy, Belgium, the UK and USA, among others. The third year of the event consolidated the institutional support of the Comunidad de Madrid, through Invest in Madrid, welcoming for the effect some of its Consejeros such as José María García Gómez, Deputy Minister for Housing, Transport and Infrastructure at the Community of Madrid.

After a private lunch that gathered the Editorial Council of Iberian Property and other guests, the Spain Real Estate Summit officially kicked-off by the hand of Josep Borrell, former EU High Representative for Foreign Affairs and Security Policy and Vice-President of the European Commission (2019–2024), who argued that global trade is not in decline, but has ceased to grow at the pace seen in recent decades, marking a phase of stabilisation in globalisation.

Geopolitics, deglobalisation and European autonomy

In his speech, introduced by Adolfo Ramírez-Escudero, Chairman of CBRE Iberia & Latam, Josep Borrell identified China as “the elephant in the room”. The Asian country, he explained, no longer occupies a central position solely in the mass production of goods, but has also gained influence in technological innovation. In this new balance, China has established itself as an industrial hub, accounting for around 30% of the world’s industrial goods, while the United States maintains its position as the main financial hub, holding nearly 60% of financial assets.

Josep Borrell linked this transformation to a deterioration in the international context. After decades in which Europe had taken peace for granted as the natural state of the world, he warned that this perception has changed and that respect for international law is at one of its weakest points.

In conversation with Adolfo Ramírez-Escudero, Josep Borrell argued that the European Union is not yet fully adapted to the new international landscape. In his view, Europe must accept that today’s world no longer fits the framework of the second half of the 20th century and prepare for a more unstable environment. This adaptation, he believes, requires developing greater military capabilities of its own and reducing its historical dependence on the United States in matters of security.

The former EU High Representative also linked strategic autonomy to productive and technological capacity. Europe, he noted, has for years benefited from the influx of low-cost Chinese goods, which has helped to keep inflation in check, but this dependence has also had consequences for its industrial base. As an example, he pointed out that the continent now produces 10% fewer cars than it did a decade ago.

In the same vein, he argued for the need to rethink the ‘just in time’ approach and move towards a ‘just in case’ approach. For Josep Borrell, Europe must rebuild its storage capacity and ensure the supply of strategic goods in the face of potential external shocks, as the pandemic has shown.

Technological dependence was another key theme of his speech. Josep Borrell pointed out that the United States maintains a dominant position in terms of access to information, data, military capabilities, satellites and digital infrastructure, a reality that constrains European autonomy. He also identified China as a key player in the energy transition, due to its control over minerals and components essential for the production of technologies such as solar cells.

The session concluded with a call to restore growth in the European Union and to approach the defence of European sovereignty from a broader perspective, encompassing security, industry, energy, technology and economic capacity.

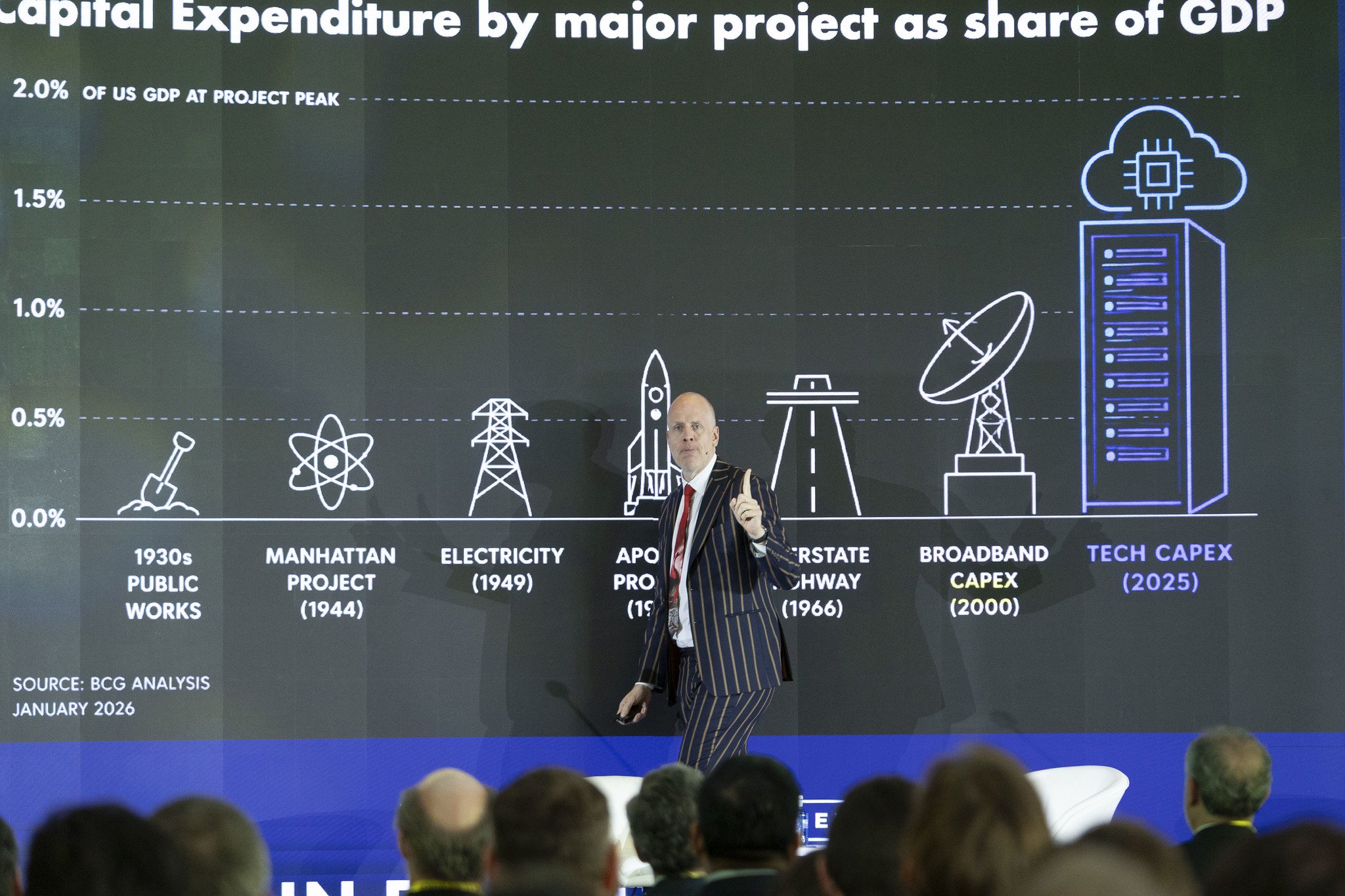

AI as a solution to the cost of waiting

The session on technology and artificial intelligence was opened by Alexandre Lima, Director of Iberian Property, and addressed the impact of AI on decision-making, productivity and business competitiveness. Magnus Lindkvist, trendspotting futurologist and author of How to Make AI Useful, argued that the current technological leap should not be understood merely as an improvement in the tools available, but as a change of scale in organisations’ ability to access, process and utilise knowledge.

Magnus Lindkvist noted that, in an increasingly technological world, “the cost of doing is falling, but the cost of waiting is rising”. From this perspective, he warned against business strategies based solely on a “wait and see” approach, as delaying the adoption of new tools can lead to a loss of competitiveness.

The expert also linked the advancement of AI to demographic change. In the major economies, falling birth rates and rising life expectancy are putting pressure on the availability of the working population and pension systems. In this context, he positioned artificial intelligence as a tool for sustaining productivity, although he qualified this by saying that neither technology nor immigration, on their own, can fully resolve the challenge.

In contrast to a defensive view of technology, Magnus Lindkvist called for an open-minded approach to the possibilities of AI. In his view, the issue is not merely about competing with it, but about using it to create. He also pointed out that it is not always the first players to enter the market who establish the strongest position, but those who learn from initial mistakes and build on previous developments.

The session concluded with a reference to Moravec’s paradox, which helps explain why some tasks that are complex for humans can be simple for a machine, while others that appear simple – particularly those requiring manual skills or physical adaptation to the environment – remain difficult to automate. In the property sector, this idea introduces an important nuance: AI does not eliminate the human dimension of the business, but it does force us to review which processes, decisions and tasks can be transformed.

Spain gains ground in the new investment cycle

The panel discussion on the economy and the new investment landscape, opened by Enrique Losantos, CEO of JLL in Spain, presented a positive outlook on the Spanish property market, albeit with variations depending on sector, strategy and risk profile. Cristina García-Peri, Senior Partner at Azora; Vanessa Gelado, Senior Managing Director and Head of Southern Europe at Hines; and Kevin Cahill, Partner and Head of European Diversified Investments at Ares RE, agreed that the price adjustment has brought fundamentals back to the fore.

Cristina García-Peri noted that the period of negative interest rates was detrimental to the property sector, as many investment decisions were based on the low cost of capital. In her view, the new cycle allows assets to be re-evaluated on the basis of their fundamentals rather than the abundance of cheap financing. “We are at the start of another major cycle for the property market,” she stated, though she ruled out the possibility that Spain is currently in a state of distress.

Speaking on behalf of Hines, Vanessa Gelado emphasised that experience in recent years has demonstrated the importance of diversification, both across sectors and across investment vehicles. Whereas the company had previously focused more on offices and retail, she explained that it now analyses a broader range of segments and structures, from core funds to strategies with greater risk exposure, with the aim of balancing the portfolio and better managing the various market cycles.

Kevin Cahill identified Spain as one of the European markets with the most favourable outlook for international capital. As he explained, the country has a lower deficit than other European economies, is maintaining growth and offers a greater diversity of opportunities. In his view, Spain is no longer a cheap market nor is it likely to become distressed, as may be the case in other European countries, but it remains attractive due to its dynamism and the breadth of possible strategies.

As for the type of opportunities, Cristina García-Peri argued that value-add in Spain should not be understood as investment in undervalued assets, but rather in underutilised markets and segments where economic growth is generating new needs, as is the case with student housing. In her analysis, alpha in Spain is being driven by fundamentals, although she cautioned that not all investors will achieve the same returns: it will be necessary to analyse each opportunity sector by sector and region by region.

Opinions differed among the speakers regarding sector selection. Cristina García-Peri identified ‘rent-to-sell’, holiday hotels, retail and logistics as among the most attractive opportunities, although she noted that the latter segment faces greater competition at European level. Regarding offices, she highlighted a need for greater caution due to the uncertainty surrounding remote working and the future impact of AI on companies’ space requirements.

Kevin Cahill highlighted the appeal of holiday hotels and BTR properties, given their potential for repositioning, and also pointed to opportunities in prime offices, retail parks and logistics. In the case of retail parks, he noted occupancy levels close to 100% in the assets in which they have invested, reflecting a lack of supply. VanessaGelado, for her part, identified retail as the main focus in Spain, followed by BTR and Grade A offices in Madrid’s CBD.

The panel concluded with a positive outlook on southern Europe and, in particular, on Spain. Cristina García-Peri highlighted that investors have stopped viewing these markets solely through the lens of their smaller size and are beginning to assess them based on the performance of their economies. Kevin Cahill described Spain as one of the most favourable markets for investors in Europe, while Vanessa Gelado argued for the need to make decisions even in turbulent environments, particularly in a context where inflation erodes the value of assets if capital remains idle.

Rethinking property value beyond price

The final session of the day, moderated by Richard Betts, Conference Chairman and Co-founder and Head of Content at Real Asset Media, prompted a discussion on how property value is being redefined against a backdrop of increased competition between asset classes, reduced macroeconomic visibility and growing demands on management.

Will Robson, Executive Director of MSCI Research & Development, noted that, in the long term, rental growth is the main driver of real estate investment appreciation. Although capital value also plays a role, he pointed out that it tends to fluctuate more over time, while income plays a more structural role in value creation. In this context, he identified Spain as one of the leading markets in Europe, both in terms of returns and transaction activity.

Brad Greenway, Head of APAC and Co-Head of EMEA Debt & Structured Finance at JLL, argued that asset-based allocation remains relevant, but emphasised that the flight to quality affects not only property but also management and investment management itself. In his analysis, operators must make decisions in an environment characterised by greater noise and uncertainty, a reality common across different markets.

From a residential perspective, Juan Pablo Vera, CEO of Testa Homes, noted that this flight to quality requires partners who understand the realities of local markets. For Juan Pablo Vera, asset quality remains a key factor, but it must be accompanied by a precise understanding of the location and the operational context.

Eduard Mendiluce, CEO of Aliseda and Anticipa, summarised value creation as a combination of acquisition and management: “The best business is to buy well and operate well”. In his remarks, he noted that acquiring an asset at the right time does not eliminate the need to optimise returns, especially in a context of higher interest rates.

Eduard Mendiluce also linked value creation to energy efficiency. As he explained, in addition to potential public subsidies, Spain has a secondary market for carbon credits that can help cover around 30% of the capital expenditure costs associated with certain energy efficiency improvement strategies.

OFFICIAL PHOTO GALLERY

Access all the photos (DAY 1) of the Spain Real Estate Summit 2026Investors celebrate the main achievements of Iberian real estate activity in 2025

And because the sector also deserves to celebrate and enjoy some relaxed networking time, the Iberian Property Investment Awards ceremony were the perfect moment to wrap-up the night. With a total of 8 categories, leading companies from Spain, Portugal, and international geographies, were recognized for their outstanding activity during 2025.

WINNERS - IBERIAN PROPERTY INVESTMENT AWARDS

Get to know all the winning projects and initiatives of the Iberian Property Investment Awards 2026Day 2 - Spain Real Estate Summit 2026

The second day of the event opened with a panel discussion on the role of REITs as investment vehicles in the new property cycle. Introduced by Dominique Moerenhout, CEO of EPRA, the session brought together Marie Cheval, Chairman and CEO of Carmila; Ismael Clemente, CEO of Merlin Properties; Tugdual Millet, CEO of Covivio Hotels; and Patrick Couttenier, CEO of Care Property Invest, in a discussion focusing on the resilience of listed real estate, adaptation to the environment of higher interest rates, and the differences between the European and US markets.

The starting point was a constructive view of the market, with expectations of a more visible recovery during the second half of the year and the observation that the sector has held up well in a context marked by uncertainty. Against this backdrop, the participants identified scale, diversification, active asset management and the ability to generate recurring cash flows as some of the factors that set listed companies apart from other real estate investment vehicles.

Marie Cheval explained that Carmila has a portfolio valued at €6.7 billion and highlighted the significance of Spain, which accounts for around 20% of its portfolio. The executive highlighted that the Spanish market has performed particularly well in terms of sales and footfall, partly due to the impact of tourism, and argued that physical retail retains a role that is difficult for e-commerce to replace, as it offers an experience linked to frequent shopping habits.

From the hotel sector, Tugdual Millet noted that Covivio Hotels manages a portfolio of around €6 billion, diversified across Europe, and highlighted the growth of the hospitality sector as a long-term structural trend. As he explained, the post-Covid recovery has consolidated the rebound in tourism demand, with visitor numbers in Europe rising by between 2% and 4%, driven particularly by the arrival of international travellers, while domestic demand remains more stable. The company plans to invest €1 billion in the repositioning of hotels and aims to continue working with the sector’s leading operators.

Patrick Couttenier outlined Care Property Invest’s position in healthcare infrastructure and care homes, with a portfolio worth €1.4 billion across four countries. The company began operations in Spain in 2020 with a €120 million portfolio, in a sector which, according to the executive, boasts high occupancy rates and growing demand linked to an ageing population. Patrick Couttenier argued that, even in times of greater uncertainty, this type of asset offers stability due to the recurring nature of care needs and the generation of sustained cash flows.

In the case of Merlin Properties, Ismael Clemente noted that the company is listed in Spain and Portugal and maintains a diversified portfolio across logistics, offices, shopping centres and data centres, a segment he identified as its main growth driver. The CEO noted, however, that data centres present significant capital barriers, ever-increasing technological demands due to the development of artificial intelligence, and a certain degree of market scepticism following years of announcements that have proved difficult to deliver. Added to this, in Europe, is a heavier bureaucratic burden.

The debate also addressed the differences between European and US REITs. The participants agreed that Europe is characterised by greater risk aversion, a more savings-oriented investment culture, a smaller scale and a more complex regulatory framework – factors that make it more difficult to raise capital compared to the US market. Ismael Clemente emphasised that regulation even limits the possibility of developing REITs specialising in certain segments, such as rural land, car parks or telecommunications towers, while MarieCheval highlighted the impact of taxation as an additional barrier to investment.

Despite these limitations, the panel concluded with a positive outlook on Europe’s ability to attract more capital, although part of that investment will be determined by capital expenditure needs and the selection of assets capable of combining scale, liquidity and stability. Looking ahead to the rest of the year, participants highlighted asset prices and geopolitical stability as two key factors to monitor.

Through five dynamic sessions, participants engaged in deep discussions across key sectors—including Retail & Logistics, Healthcare & Senior Living, Offices, Data Centers, and also a dedicated session to Madrid major urban developments—highlighting Spain’s adaptability to meet emerging demographic, technological, and economic demands.

1.Retail and Logistics: Selective Growth and Disciplined Capital Allocation

Chaired by Tom Waite, Director of Industrial and Logistics Investment, International Capital Markets EMEA at JLL, and Sandra Ludwig, Head of Retail Investment EMEA at JLL, this session explored how both sectors are entering a more selective phase of the cycle. While logistics remains a major European asset class, opportunities in Spain were described as increasingly focused on specific locations and asset quality, particularly in Madrid, Barcelona and Valencia. Retail, by contrast, is regaining momentum as strong operational performance, tourism and consumer fundamentals support renewed investor confidence. The discussion highlighted that Spain continues to offer attractive dynamics, although capital deployment requires greater discipline, detailed market analysis and a selective approach to avoid oversupply risks.

2.Healthcare and Senior Living: Long-Term Demand Meets Development Constraints

Led by Nuria Ochoa, Senior Director of Healthcare and Life Sciences at CBRE, this session examined how healthcare and senior living continue to strengthen their institutional profile as demographic trends reinforce long-term demand. Participants highlighted the sector’s ability to combine stable income streams with social impact, particularly in assets linked to ageing populations and care provision. While Spain remains attractive relative to other European markets due to pricing and yield levels, development challenges and rising costs continue to constrain the pace of new supply. The discussion underlined that long-term fundamentals remain strong, although growth increasingly depends on overcoming structural barriers to delivery.

3.Offices: Improving Fundamentals Support a Gradual Recovery

Chaired by Juan Barba, Senior Advisor at B Living (Grupo Barba), the office session focused on the sector’s improving outlook after several years of uncertainty. Participants agreed that demand for high-quality space remains strong across Iberia’s main cities, with supply shortages supporting rental performance in prime assets. However, despite improving sentiment and stronger market conditions compared to recent years, investors continue to adopt a more selective approach than in previous cycles. The discussion highlighted that the sector is moving into a more favourable phase, although perceptions around office investment have not yet fully returned to pre-pandemic levels.

4.Data Centres: Power Availability Becomes the New Competitive Driver

Moderated by Francisco Porras, Head of the DC Business Unit at Merlin Properties, this session examined the rapid evolution of digital infrastructure and the changing requirements behind data centre development. As artificial intelligence and cloud computing drive unprecedented demand, energy access has emerged as the primary challenge, replacing traditional concerns around location alone. Participants discussed how future infrastructure will require greater technical specialization, flexibility and long-term planning to avoid technological obsolescence. The session highlighted that digital growth will increasingly depend on the capacity to deliver highly adaptable infrastructure capable of supporting evolving computing needs.

5.Madrid’s Mega Developments: Building Integrated Cities at Scale

Chaired by Patricia Gross, Business Development Manager for Spain at Sonae Sierra, this session focused on Madrid’s capacity to deliver large-scale urban transformation projects. Rather than concentrating solely on housing supply, the discussion highlighted a broader vision centred on creating integrated neighbourhoods combining residential, office, retail and community uses. Public-private collaboration was identified as a key success factor, alongside the confidence generated by increasingly agile planning processes. Participants concluded that Madrid is positioning itself as a benchmark for large-scale urban development, demonstrating how mixed-use environments can support both investment attractiveness and long-term city growth.

Living: operation, scale and flexibility mark the residential convergence

The session “Living. From flex to multifamily” analysed the convergence between flex living, co-living, PBSA and traditional multifamily, in a context where the boundaries between formats are becoming less rigid. It began with a keynote speech by Laurent Ternisien, Deputy CEO of Investment Management and CEO of Luxembourg at BNP Paribas REIM, before giving way to a panel of investors moderated by Richard Betts, Conference Chairman and Co-founder and Head of Content at Real Asset Media, featuring Carlos Zucchi, Managing Partner and CEO of Argis; Carlo Matta, CEO of Nido; and Laurent Ternisien himself.

The starting point was the size of the residential rental market in Spain. Although the country has a lower proportion of tenant households than other European markets, there are 2.9 million families living in rented accommodation, of whom 526,000 are in Madrid, 523,000 in Barcelona and 142,000 in Valencia. In this context, residential property was presented as an asset class capable of supporting people through different stages of life and opening up investment opportunities across formats with varying levels of risk, return and operational specialisation.

During the session, it was noted that flex living can offer a higher potential return, but also involves greater risk and increased complexity in underwriting. One of the trends identified is that some investors are no longer simply buying the property asset, but are also taking stakes in the operator, a decision that reflects the growing importance of management in value creation.

Carlo Matta argued that the operation is key to maximising the value of the property asset, particularly in flex living, where a good operator enables costs to be controlled, services to be tailored, and the data generated by the management itself to be used to analyse future investment opportunities. In the same vein, Carlos Zucchi noted that scale is a second fundamental element, as the temptation to project higher revenues can be accompanied by higher costs as well, which requires maintaining a balance between expected profitability and operational structure.

The panel also addressed the convergence between PBSA and flex living in terms of services and facilities. Although the degree of sophistication varies depending on the segment and the customer profile, the participants agreed that the foundations of both models tend to be converging. Laurent Ternisien added that flexibility is not a static concept, as it changes over time depending on how residents’ uses and needs evolve.

Carlos Zucchi illustrated this transformation using the example of residences in Spain, where ground-floor spaces designated as canteens have lost importance due to changing consumption habits and the growth of platforms such as Uber Eats. This type of evolution requires a review of the design and allocation of space within the properties.

The PBSA was described as an established sector capable of attracting new waves of capital, while flex living was presented as an attractive asset class but one that is still not fully understood by some risk-averse investors. The main challenge, it was argued, lies in the supply: many existing or under development assets are situated on commercial or hotel land, which means they compete with office or hotel projects. Despite the evolution of these formats, the panel agreed that location remains a fundamental factor in identifying good investment opportunities.

OFFICIAL PHOTO GALLERY

Access all the photos (DAY 2) of the Spain Real Estate Summit 2026A warm THANK YOU to our Partners

Iberian Property would like to take the chance to recognize all the companies and entities who supported the Spain Real Estate Summit this year, and which hopefully will continue contributing to the success of such an initiative:

CBRE, JLL, Invest in Madrid & Comunidad de Madrid, Merlin Properties, ARGIS, Crea Madrid Nuevo Norte, HLRE socimi, Aliseda, Testa Homes, Sonae Sierra, Constructora San José, Azora, Izilend, Nhood, Square Asset Management, and Clifford Chance.

A word of appreciation as well for all the industry partners who accompanied us: Real Asset Media, ACI, APRESCO, AECC, ASPRIMA, EPRA, ULI Spain, APPII, SQUARE and Simed.